Credit Demand vs. Stimulus: China’s January Lending Surge Still a Miss

Daniel Kassim

Finance Writer

Banks in China have extended a large amount of credit in January. On the face of it, it is a very impressive performance. However, if one were to dig a little deeper, there is a lot more to it than what meets the eye.

The new yuan loans in January were 4.71 trillion yuan. This is very close to five times the December levels of 910 billion yuan. This is a very rapid spurt. However, this is also a miss on the expected levels, as analysts had expected 5 trillion yuan in January 2026, and the actual number for January 2025 was 5.13 trillion yuan. This is also a decline from the same period last year.

This is the paradox that exists in the credit situation in China now. The money is flowing, but not as rapidly as it should, and not from the right sources either.

The Numbers You Need to Know

The People’s Bank of China has released a set of numbers that are quite mixed. Here are the key numbers that caught our attention:

The aggregate financing, which is a measure of the credit extended to the economy in the form of bonds, trust loans, and other instruments, came in at 7.2 trillion yuan. This beat the median forecast of 7.1 trillion yuan in a Bloomberg survey. Not bad, so far.

However, the new yuan loans in January were 4.71 trillion yuan, which failed to meet the market consensus of 5 trillion yuan. The growth of outstanding yuan loans was 6.1% year-over-year in January, which marked a record low and declined from 6.4% in December. It was expected to be 6.2%.

M2 money supply growth was 9.0% year-over-year, much stronger than the expected 8.4%. The narrower definition of money supply grew 4.9%, which was up from 3.8% in December. Total social financing grew 8.2% year-over-year, slightly slower than 8.3% in December.

What these numbers mean collectively is this: the broad credit outlook was positively impacted by the sale of government bonds and fiscal transmission channels, but the actual loans to the non-bank sector were weak. The government’s credit is carrying more weight. The private credit demand is not keeping up with the pace.

Why Loans Missed

January is always a strong month for Chinese loans. Banks front-load their books at the start of the year, competing for the best customers and gaining market share early. This is a real and well-known phenomenon.

However, 2026 presented a twist. The Spring Festival falls in mid-February this year, instead of late January, which means that some business activities and short-term borrowing needs of corporations took place in the following month. This is a timing difference, but not the entire explanation.

According to Zhou Hao, the chief economist at Guotai Junan International, “The share of new loans to total social financing has been below 50% for most of the second half of 2025. This trend continued into January 2026. This means that financing, which is now fueling credit growth, is no longer led by bank loans but by financing that is guided by the government. This is set to continue in 2026, with the fiscal deficit likely to stay above 4% of GDP.”

Corporate loans rose to 4.45 trillion yuan from 1.07 trillion yuan in December, which looks positive at first glance. Consumer loans, including mortgages, rose 456.5 billion yuan after declining to 91.6 billion yuan in December, which is a positive development. However, the overall lending amount is still not sufficient to satisfy the conditions to show a true recovery in demand.

The Deeper Problem: Demand Itself Is Weak

This is what the credit statistics cannot adequately tell you but is the reality: Chinese consumers and enterprises simply do not want to borrow money.

It is not a liquidity issue. The PBOC has the leeway to ease monetary policy further. The 1-year and 5-year loan prime rates have been held at 3% and 3.5% for eight months running. The central bank has signaled that it still has room to reduce reserve requirement ratios and policy rates. It is not a liquidity issue.

It is a confident issue.

China has been stuck in a deflationary feedback loop for three years. Property prices have declined by an estimated 85% of the value of peak prices since 2021. There are approximately 80 million unsold or vacant homes in the country. Households that have witnessed their primary asset decline in value are not likely to take out new loans. Instead, they save and pay off existing mortgages ahead of schedule.

Household credit growth saw record lows in 2025, with outstanding growth of only 1.1% year over year in November. Total new bank loans in 2025 were 16.27 trillion yuan, a seven-year low. Retail sales growth was down sharply from 6.4% in May 2025 to only 1.3% in November. E-commerce sales on major platforms such as Taobao and JD.com were down 4.3% year to date as of last year.

A similar math problem exists for businesses. Overcapacity has resulted in price wars in different industries, which has further resulted in lower profits and lower incentives for investment. With lower profits and uncertain demand, you do not borrow more. You cut costs.

Gene Ma, China Research chief at the Institute of International Finance, was very candid about it: “China’s core problem is the lack of demand. The collapse of investment outpaced the collapse of consumption in 2025, which is very concerning.”

Government Bonds Are Carrying the Load

The beat on aggregate financing came almost entirely from the government’s bond issuance. Beijing has been front-loading its bond issuance to fund infrastructure spending and stimulate the economy, which pushed the broad credit measure even as private lending growth was disappointing.

This is a direct consequence of how one is supposed to interpret the top-line numbers. If fiscal expansion is driving credit growth while private loan demand growth is stagnant, it’s not a sign of an organic recovery. It’s a sign of fiscal expansion papering over cracks.

Julian Evans-Pritchard of Capital Economics was spot on. “Fiscal policy last year was sufficient to enable the PBOC to stand by and do nothing. But now that the fiscal policy is likely to be less expansionary in 2026, the PBOC will have to work harder to ensure that credit and the economy are not growing too slowly.”

The trouble is that the government has not suggested a target for the budget deficit in 2026. If fiscal expansion continues to slow down and the private sector does not pick up the slack, credit expansion could slow down again in the coming months. As Capital Economics Zichun Huang said, “The current trajectory means that monetary policy will not be able to support the economy.”

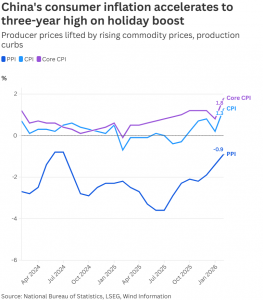

Deflation Raises the Real Cost of Borrowing

This is a point that gets lost in the debate about the nominal interest rate. Even if the PBOC lowers interest rates, the real cost of borrowing is still high because of deflation.

(Courtesy of CNBC)

The consumer price index in China has not gone up for three years. Producer prices have been negative. When you borrow at 3% and prices are falling at 0.5%, your real cost of borrowing is 3.5%. Lowering interest rates is helpful, but it does not address the real rate problem if deflation continues.

This is why the IMF has called on China to implement faster fiscal expansion and structural reforms rather than focus on interest rate policies. The Fund expects 4.5% GDP growth in 2026, down from 5% in 2025, and says that “domestic demand and deflationary pressures remain important risks.”

The World Bank expects 4.4% growth in 2026. A Reuters poll of economists also expects 4.5% growth. China’s economy grew 4.5% year over year in the fourth quarter of 2025, the lowest since the post-COVID reopening in late 2022.

What Policymakers Are Doing About It

Beijing has not sat still. In January, the PBOC cut interest rates on targeted sector loans and announced that it would set up a dedicated relending facility just for private firms. It has also increased quotas for tech innovation loans, has plans to increase support for small and medium-sized enterprises, and lowered the minimum down payment ratio for commercial property mortgages to 30%.

The government has been vocal about its ambitions to encourage more domestic consumption, although it has been noted that most of these policies are still supply-side policies and do not do anything to fill the income and confidence gap that households face today. Six ministries released a broad policy plan to promote the growth of consumer sectors in December, aiming to reach the trillion-yuan mark in the electronics and sporting goods sectors by 2027. Goldman Sachs analysts noted that there was no funding mechanism or implementation plan, and that this policy is purely supply-side and does not address the demand issue at all.

PBOC Deputy Governor Zou Lan said that there is still room to maneuver reserve requirement ratios and policy rates. This is significant because the yuan has appreciated by over 1% against the dollar in the last month, giving policymakers some room to maneuver without having to worry about capital outflows or a weakening currency.

The big question for 2026 is whether the fiscal injection, credit policies, and subsequent monetary policy easing will be sufficient to instill confidence in the private sector. Not just the amount of lending above the previous month, but organic demand from businesses investing in growth and households confident enough to spend.

What to Watch Going Forward

You will want to keep an eye out for a few key metrics in the coming months to see if the Chinese credit recovery is real or state driven.

First, keep an eye on the share of loans in total social financing. If this number stays below 50%, it means that bonds are still fulfilling the role that loans should be. A real recovery will be seen when this number goes up.

Second, keep an eye on credit to households. Demand in the housing market and consumer loans are the best way to see if the housing market and consumer sentiment have stabilized. A month of data is not indicative of a trend, especially after the drop in December.

Third, keep an eye on M1 growth. The tighter measure of money supply is a function of the amount of money actually in the system. The 4.9% increase in January from 3.8% in December is a small positive sign, but you have to see this trend continue and build on it.

Fourth, keep an eye on what the PBOC decides to do next. A reserve requirement cut or a policy rate cut in the first half of 2026 would show that policymakers are serious about the slowdown, not just talking about it.

Finally, keep an eye on the upcoming annual parliamentary session in March. Beijing will announce its 2026 growth target and any new fiscal policies at this time. A target of around 5% is expected, but this will be achieved either through a strong rebound in private demand or another round of government spending to fill the void left by it.

The Bottom Line

The January lending data is a Rorschach test for the Chinese economy. You can look at the 7.2 trillion-yuan aggregate financing number and see a country that beats forecasts. Or you can look at the record low outstanding loan growth rate and below-forecast new lending number and see a country where domestic credit demand is still a problem.

Both are right. That’s the rub.

The Chinese stimulus policies are doing well enough to keep the economy from falling apart, but not well enough to get the kind of private sector-led momentum that drives growth. The government bonds are supporting the aggregate numbers. Households are still skittish. Businesses are still cautious. The real estate market is still a drag on the economy.

For investors and entrepreneurs trying to make sense of the Chinese economy, the January data is not a crisis. But it’s not a green light either. The gap between the kind of credit that Beijing is trying to inject into the economy and the kind of credit demand that the economy needs is what tells you that the underlying confidence problem has not been solved. Until it is, every month’s lending data will show you the same thing: numbers that are better than December but not good enough to get China to where it needs to be.

Contact Daniel at daniel.kassim@student.shu.edu