Separating Headlines From Reality: What Risk is Actually Rising in Private Credit?

Thaddius Gamueda

Head Finance Editor

In 2007, the housing market looked unstoppable. Prices were rising, capital was flowing, and the headlines were focused on how much money was being made. What nobody was watching closely enough was the math underneath — the adjustable rate resets, the coverage gaps, the assumptions that only worked if nothing went wrong. We know how that ended.

Private credit is not the housing market. But the pattern of focusing on size over stress is the same. As of 2024, private credit has grown into a $1.7 trillion asset class and is on pace to reach $2.6 trillion by 2029 according to Preqin. Record fundraising. New bank partnerships. AUM milestones every quarter. The story sounds simple: more money, more deals, more momentum.

But as someone who has spent time building financial models and analyzing performance across industries, I have learned that the most important signals rarely show up in the headline number. They show up in the math underneath. Right now, there are two risks in private credit that I believe are not getting nearly enough attention: coverage ratios deteriorating quietly at the borrower level, and the growing connection between private credit and the traditional banking system. One tells you where stress is building. The other tells you why it matters more than it used to.

What Is Private Credit and Why Has It Grown So Fast?

Private credit refers to loans made by non-bank lenders. Think direct lenders, private equity-backed credit funds, and alternative asset managers like Blue Owl Capital, Ares, and Apollo — directly to companies, usually middle market businesses that are too small or too complex for the public bond market. Unlike a bank loan or a traded bond, these deals are negotiated privately, held to maturity, and not easily sold.

The asset class exploded after 2008 when banks pulled back from risky lending due to new regulatory requirements. Private lenders stepped in and filled the gap. For over a decade, low interest rates made borrowing cheap and coverage ratios looked healthy across the board. Investors loved the floating-rate income and the premium over public credit. Everyone won.

Then rates rose. And that is where the real pressure started building.

Why Coverage Ratios Are the Most Underappreciated Risk Right Now

This is the signal I am most focused on. When interest rates rise, interest expense rises immediately. But operating improvements take time. That timing mismatch is where damage accumulates quietly, before any default shows up in a headline.

The cleanest early warning is cash interest coverage — how many times over a company can cover its interest payments with its operating cash flow. When that number slides toward 1.0x, companies lose flexibility fast. One weak quarter becomes a liquidity problem. A small revenue miss forces a cut to capital expenditures. A pricing increase gets delayed. What starts as a temporary margin squeeze becomes permanent.

Credit researchers have pointed out that a meaningful subset of private credit borrowers have been operating with very thin coverage as rates stayed elevated. These are not companies that are defaulting. They are companies that are surviving — but barely, and with less and less room for error. That is the soil where problems sprout first.

Most market participants are focused on default rates, which are a lagging indicator. By the time defaults spike, the stress has been building for months. The investors and analysts paying attention to cash interest coverage right now are the ones who will not be surprised when the defaults eventually show up.

What to watch:

- Cash interest coverage trending down quarter over quarter

- Free cash flow after interest, not just EBITDA growth

- Revenue concentration — coverage breaks faster when the top line slips

How EBITDA Add-Backs Make Stress Disappear on Paper

Here is the uncomfortable truth about why coverage can look fine on paper while the business is struggling in real life. A lot of it comes down to add-backs.

EBITDA add-backs are adjustments that sponsors and borrowers make to reported earnings — cost savings that haven’t happened yet, synergies from an acquisition, one-time expenses that keep recurring. In moderation, they are a reasonable part of credit analysis. In excess, they are a fog machine. S&P Global’s work on this topic has shown how aggressive add-backs inflate projected leverage and make deals look safer than they end up being.

In a low-rate environment, this was manageable. The margin for error was wide. In today’s environment, when interest costs are high, you cannot afford fantasy EBITDA. You need cash generation that actually arrives on time. When coverage is already thin and the EBITDA number being used to calculate it is inflated, the real picture is worse than what most people are seeing.

What to watch:

- Whether add-back categories are capped or unlimited

- The adjusted EBITDA bridge — is the adjustment line growing over time

- Whether synergies and cost savings require proof or are taken on faith

Covenant Slippage: The Protection That Is Not Protecting

Covenants are legal protections written into loan agreements that give lenders an early warning when a borrower is struggling. A maintenance covenant, for example, might require a borrower to maintain a minimum coverage ratio. If they breach it, the lender gets notified and can take action before things get worse.

The problem is not that covenants have disappeared entirely. It is that they have been quietly watered down to the point where they barely function as intended. Cushions get wider. Definitions get looser. Cure rights become more forgiving. Baskets expand. The label stays on the loan, but the early warning system has been removed.

You do not need to be a lawyer to track this. You just need to ask one question: if this borrower’s performance starts to drift, do the lenders find out early enough to do something about it — or do they find out when it is already too late?

What to watch:

- Maintenance covenant tightness — not just whether covenants exist, but whether they have teeth

- Cure rights and how frequently they are being used

- Builder baskets and leakage terms — how easily value can leave the collateral package

Amend-and-Extend: When Flexibility Becomes a Cover Story

In a normal credit cycle, stress shows up as defaults. In the current higher-rate environment, it is showing up as time. Borrowers who cannot refinance their loans at current rates are instead getting extensions — maturity pushes, covenant resets, pricing step-ups. The loan stays alive. The stress gets quietly deferred.

This is one of the advantages private markets have over public ones. There is no forced mark-to-market. A private lender can sit across the table from a struggling borrower and negotiate a solution instead of triggering a default. In many cases, that flexibility genuinely saves businesses and protects investor returns.

But when amendments become frequent — especially repeat amendments on the same borrower — they stop being a tool for managing temporary turbulence and start being a signal that the coverage math is not working. The key question to ask is whether the amendment is paired with a real operating improvement plan or whether it is just buying time.

What to watch:

- Rising amendment frequency, especially repeat amendments on the same borrower

- The cost of extension — fees, spread increases, additional collateral, warrants

- Whether amendments come with credible operating plans or just a longer runway

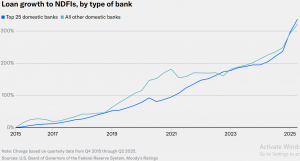

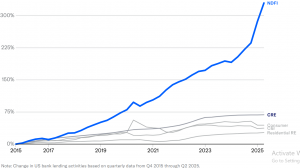

The Risk Nobody Is Talking About: Private Credit Is No Longer Isolated

Here is the second risk I think deserves far more attention — and the one that changes the stakes of everything else on this list.

The original private credit narrative was simple: nonbank lenders make loans, hold them, and collect income. No public market exposure. No systemic risk. Stress stays contained. That narrative has been a big part of why the asset class attracted so much capital over the past decade.

But that story is quietly becoming outdated. Banks are increasingly tied to private credit through lending facilities and financing lines. They are providing the capital that private lenders then deploy into deals. The Boston Fed has raised explicit concerns that these growing connections could become a financial stability issue in a severe downturn, especially when transparency across the system is limited. FSOC has similarly flagged the challenges created as more lending migrates outside the traditional banking system in ways that are difficult to monitor.

Think about what this means practically. If coverage ratios deteriorate broadly across a vintage of deals, the stress does not stay neatly inside private credit funds. It travels through the financing lines back to the banks that provided them. The system that was supposed to be insulated turns out to be more connected than the headline narrative ever acknowledged.

Private credit is not about to blow up. But the assumption that it operates in a clean, contained silo is no longer accurate. And the coverage ratio problem and the interconnectedness problem are not two separate risks — they are the same risk at two different scales.

What to watch:

- Bank exposure to private credit through lending facilities and financing lines

- Transparency and disclosure quality from major direct lenders

- Whether stress in private credit deals begins showing up in broader bank credit conditions

- Regulatory commentary from the Federal Reserve, FSOC, and OFR on nonbank financial institutions

What Should Investors and Students of Finance Do With This?

None of this means private credit is a broken asset class. Far from it. The flexibility, the floating-rate income, and the access to middle market companies that public markets cannot reach are all real advantages. The best managers in this space — the ones underwriting carefully and watching their coverage math — are going to continue to deliver strong returns.

But the market is at a point where documentation, definitions, and refinancing mechanics matter as much as credit selection. The investors who stay ahead of this cycle will be the ones tracking cash — not just AUM. They will be reading the credit agreements, not just the pitch decks. They will be watching amendment frequency the same way equity investors watch earnings revisions.

Whether you are an investor, a student of finance, or someone paying attention to where capital is flowing in today’s market, these are the signals worth building into your framework. The headline numbers will tell you who is winning the fundraising race. The cash flow and the credit terms will tell you who is actually underwriting responsibly.

Track cash. Track terms. Track amendments. And pay close attention to who is financing the financiers.

Contact Thaddius at gamuedth@shu.edu